Shares of Page Industries Ltd on Friday tumbled 15 per cent to a low of ₹34,968.60 on the BSE, as the company reported a 58.87 per cent decline in net profit at ₹78.35 crore for the fourth quarter ended March 31 due to higher cost of inventory and lower capacity utilisation.

Its revenue from operations was down 12.78 per cent to ₹969.09 crore (₹1,111.11 crore).

However, the stock recovered partly to close at ₹37,456.25 — down nine per cent over the previous day’s close of ₹41,139.50.

For the fiscal ended March 2023, the brand licensee of Jockey underwear’s net profit rose 6.46 per cent to ₹571.24 crore (₹536.53 crore) and revenue from operations was up 23.21 per cent to ₹4,788.63 crore.

‘Temporary impact’

The company’s Managing Director VS Ganesh said the year was a challenging one with a general decrease in consumption. He considers this impact to be temporary and maintains a positive outlook on demand. However, analysts are disappointed with the performance and see challenging days ahead.

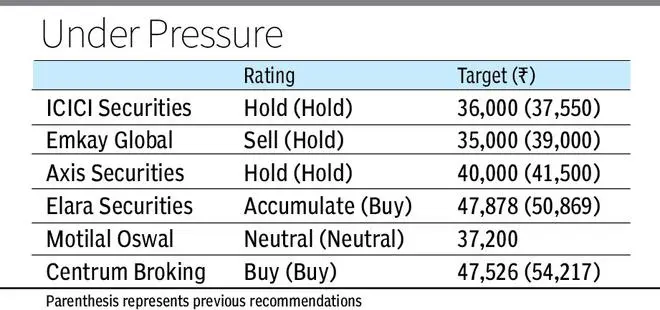

According to Emkay Global Financial, which advised ‘Sell’ on the stock with a target price of ₹35,000, said Q4 PAT was 40 per cent below estimate, led by an all-round miss.

Page Industries expects margin to keep on the recovery path, with realisation of low-cost inventory and focus on cost savings (besides marketing). “But we believe revenue recovery is paramount for retracing margin to the targeted 19-21 per cent band (vs. 15 per cent in H2FY23).”

Axis Securities said: “We like the management’s undeterred focus on distribution expansion across channels and smaller towns, coupled with a strong stance on the implementation of ARS across its retail network despite near-term volume pressure. It will make Page more agile and stronger than the competition in the long run. However, near-term challenges such as a subdued demand environment and implementation of ARS will keep the volume growth and margin trajectory on the sidelines.”

Elara Securities said, “We believe Page Industries is deriving robust operating leverage from the strong recall of its brand, Jockey. We expect near-term pressure on account of ARS implementation to be offset by benefits derived from a strengthened business model.”

The stock price has been under pressure over the last six months and declined more than 20 per cent. “Due to rich valuations (58x FY25E) and moderate growth outlook (owing to increased competitive intensity), we believe the stock price does not offer upside,” said ICICI Securities.

![]() Comments

Comments

Comments

Comments have to be in English, and in full sentences. They cannot be abusive or personal. Please abide by our community guidelines for posting your comments.

We have migrated to a new commenting platform. If you are already a registered user of TheHindu Businessline and logged in, you may continue to engage with our articles. If you do not have an account please register and login to post comments. Users can access their older comments by logging into their accounts on Vuukle.