Liquidity in the banking system has swung into deficit mode after remaining in surplus mode for almost 40 months.

The change in the liquidity situation has come due to advance tax outflows for the second quarter. This also nudged up call money rate temporarily above the repo rate.

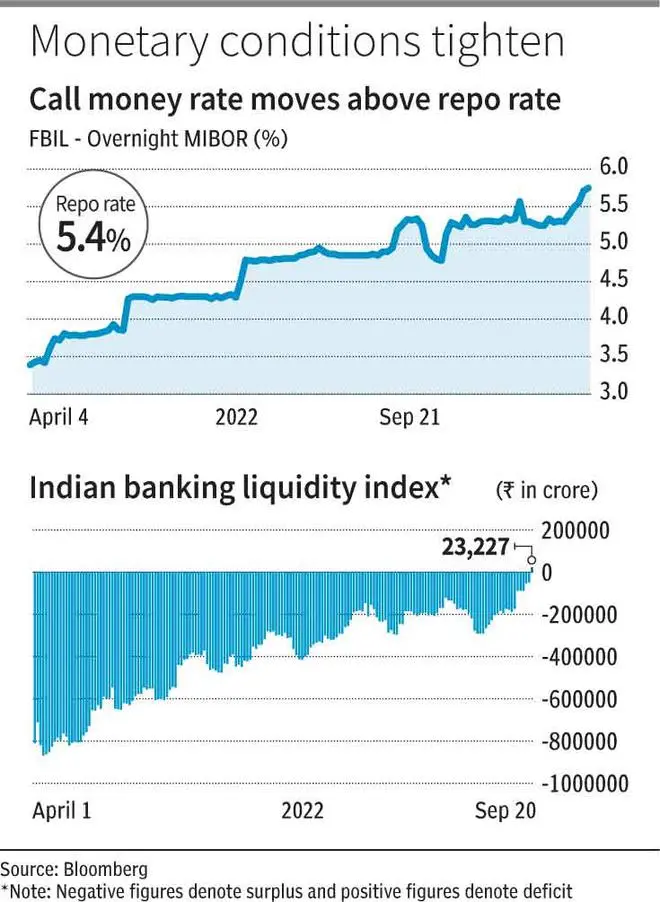

Liquidity deficit in the banking system was estimated at ₹23,227 crore on Wednesday against previous day’s surplus of ₹ 47,936 crore, per Bloomberg data.

Call money rate up

Consequently the interbank call money rate rose above the repo rate (of 5.40 per cent) to touch a high of 5.85 per cent due to liquidity deficit, before cooling off to last trade at 5 per cent (previous day’s last traded rate: 4.40), according to CCIL data.

To help the banking system tide over the liquidity deficit and also soften call money rates, the Reserve Bank of India said it will conduct a ₹50,000-crore Variable Rate Repo (VRR) auction of one-day tenor under Liquidity Adjustment Facility on Thursday.

According to V Lakshmanan, Head of Treasury, Federal Bank: “Right now there is a bit of a deficit situation. In the last one week, advance tax outflows have happened. Further, Goods and Service Tax related outflows will be happening.

“When this money comes back into the system, the situation will get reversed. The liquidity deficit is a transient situation at this particular point in time.”

He said that right now the liquidity deficit is an event driven action, which is a temporary situation that will get reversed.

Lakshmanan observed that there has been a small move up in the call money rates due to the liquidity deficit.

Referring to VRR auction announcement by RBI, he said this is a logical response to the liquidity situation.

Dipanwita Mazumdar, Economist, Bank of Baroda, opined that in the coming months, pressure on liquidity would continue from RBI’s forex intervention, capital spending of the government as also pickup in currency demand.

“With credit growth already running at double digit, it would add further pressure on the liquidity numbers.

“Short-term rates thus would increase at a faster pace as the direct reflection of tighter liquidity and RBI’s rate hike would be on these papers,” she said.

T-Bill rates rise

On short-term rates, Mazumdar observed that Treasury Bill (T-Bill) rates have started inching up since RBI stepped on to the path of rate hike cycle.

“With the frontloading of RBI’s 140 basis points rate hike till date, T-Bill yields have started rising. In comparison to April 2022 cut off yield, the average cut off yield across all (T-Bill) tenors rose by 179 bps, while for 10Y Government Security yield the increase is only 31 bps,” she said.

Thus, the borrowing cost for short-term papers is increasing at a faster pace compared to longer tenor securities.

.

![]() Comments

Comments

Comments

Comments have to be in English, and in full sentences. They cannot be abusive or personal. Please abide by our community guidelines for posting your comments.

We have migrated to a new commenting platform. If you are already a registered user of TheHindu Businessline and logged in, you may continue to engage with our articles. If you do not have an account please register and login to post comments. Users can access their older comments by logging into their accounts on Vuukle.