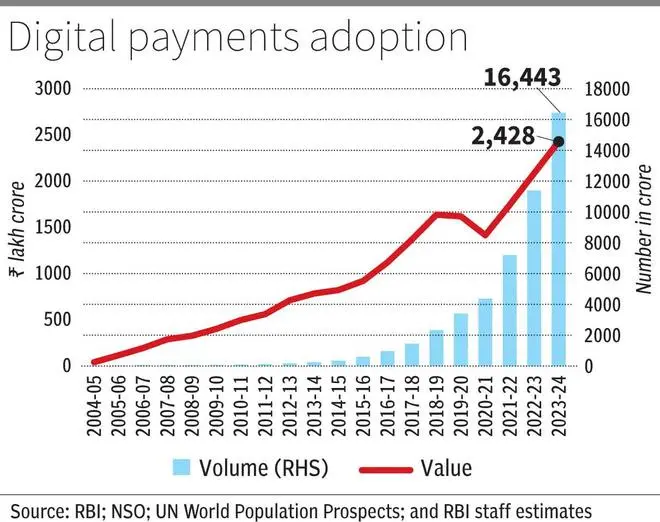

Digital payments have recorded a compounded annual growth rate (CAGR) of 50 per cent and 10 per cent in volume and value terms, respectively, in the last seven years (between 2017-18 and 2023-24), RBI said in its latest Report on Currency and Finance (RCF).

Digital payments, including NEFT (National Electronic Funds Transfer), UPI (Unified Payments Interface), credit and debit cards, saw 164 billion transactions worth ₹2,428 lakh crore in 2023-24. Except paper-based instruments, all other payments constitute digital transactions.

Share of NEFT

In value terms, NEFT transactions had the highest share (49.4 per cent) in total retail payments in 2023-24, followed by UPI (25.3 per cent share in 2023-24 as compared to only 2.4 per cent in 2018-19).

RBI officials noted that UPI has seen a tenfold increase in volume over the past four years, increasing from 12.5 billion transactions in 2019-20 to 131 billion transactions in 2023-24 - 80 per cent of all digital payment volumes.

Currently, the UPI is recording nearly 14 billion transactions a month, buoyed by 424 million unique users in June 2024.

The officials said the surpassing of UPI transactions volume for peer-to-merchant (P2M) transactions over the peer-to-peer (P2P) segment and high volume for small value transaction categories indicate its high usage.

Governor Shaktikanta Das, in his foreword to RCF, underscored that digitalisation in finance is paving the way for next-generation banking; improving access to financial services at affordable costs; and enhancing the impact of direct benefit transfers by effective targeting of beneficiaries in a cost-efficient manner.

Retail loans

Further, loans in the retail segment are being enabled by online payments and innovative credit assessment models with instant disbursements. E-commerce is being boosted through embedded finance. All these innovations are making financial markets more efficient and integrated

“....At the same time, digitalisation also presents challenges related to cybersecurity, data privacy, data bias, vendor and third-party risks, and customer protection. Increased inter-connectedness may lead to systemic risks.

“Additionally, emerging technologies can introduce complex products and business models with risks that users may not fully understand, including the proliferation of fraudulent apps and mis-selling through dark patterns. Digitalisation may induce human resource challenges in the financial sector, necessitating strategic investments in upskilling and reskilling,” Das said.

RBI officials highlighted that the intensity of digital payment usage has shot up multi-fold: the number of transactions per lakh (Rs) of GDP increased from 0.8 in 2005-06 to 56 in 2023-24, and the number of transactions per capita from 0.2 in 2005-06 to 114 in 2023-24.

The average value of transaction per capita for total digital payments surged from ₹0.4 lakhs to ₹16.8 lakhs over the same period.

![]() Comments

Comments

Comments

Comments have to be in English, and in full sentences. They cannot be abusive or personal. Please abide by our community guidelines for posting your comments.

We have migrated to a new commenting platform. If you are already a registered user of TheHindu Businessline and logged in, you may continue to engage with our articles. If you do not have an account please register and login to post comments. Users can access their older comments by logging into their accounts on Vuukle.