The Reserve Bank of India (RBI) may up the risk weights on unsecured personal loans and outstanding on credit cards to tamp down the strong growth in these segments and curb potential bad loans.

Bankers say while the going is currently good on the unsecured personal loans and credit cards front due to robust demand, the fear is that during times of distress, non-performing assets will show up, which could hit banks. So, they expect some “action” on risk weights from the central bank.

Higher risk weights will moderate banks’ ability to lend to the unsecured personal loans and credit cards segments as capital charge will go up. Currently, the the risk weight on unsecured personal loans and outstanding on credit cards is 100 per cent and 125 per cent, respectively. Risk weights are percentage factors that adjust for the credit risk of different types of assets.

Also read: Statistalk. Personal loans: What makes them popular among Indians?

Loan provisioning

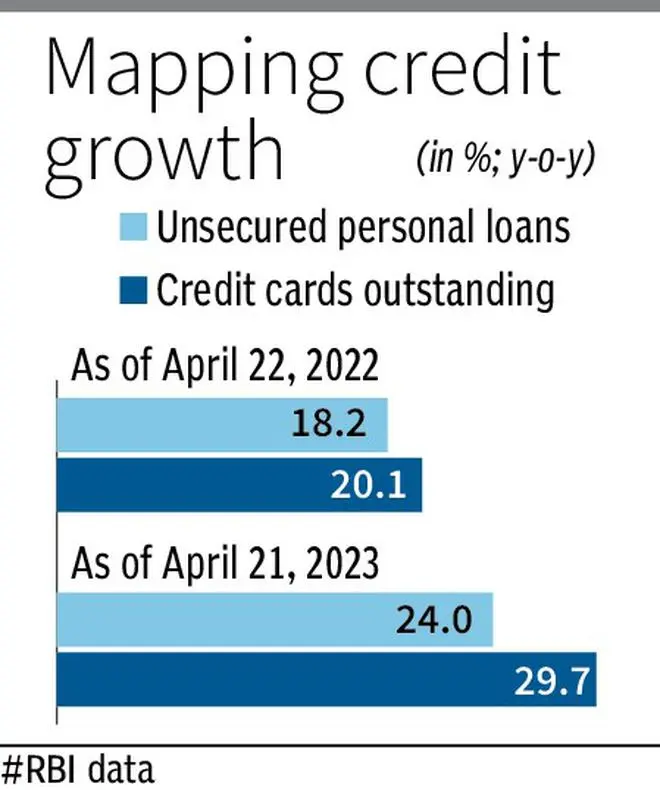

According to RBI data, unsecured personal loans grew 24 per cent y-o-y as on April 21, 2023, compared with 18.2 per cent y-o-y growth as on April 22, 2022. Credit card outstanding, too, grew 29.7 per cent y-o-y as on April 21, 2023, compared with 20.1 per cent y-o-y growth as on April 22, 2022.

“If an unsecured personal loan goes bad, straight away the loss is 100 per cent. In the first year of the loan not being serviced, a bank may provide 25 per cent, but in the second year, it has to be fully provided. In some banks, in the first year itself, 100 per cent provisioning is done for unsecured loans,” said a top private sector bank official.

The official observed that when the risk weight is increased, capital gets consumed. So, higher capital will need to be allocated to make these loans. So, to that extent, the ability lend further gets moderated.

Credit growth

Care Ratings, in a recent report, said unsecured loans (other personal loans + credit card outstanding + consumer durables) reported a robust growth of 25 per cent y-o-y in April 2023 due to the granularisation of credit, digitalisation of loans, preferences for premium consumer products and the credit push by banks.

Unsecured loans’ share increased to 32.9 per cent in the personal loans segment as on April 21, 2023, compared with 31.4 per cent over a year ago. After housing, unsecured loans is the second biggest component in the personal loans segment. Given the strong demand for different retail loan verticals, the agency expects retail credit growth to remain robust for FY24.

![]() Comments

Comments

Comments

Comments have to be in English, and in full sentences. They cannot be abusive or personal. Please abide by our community guidelines for posting your comments.

We have migrated to a new commenting platform. If you are already a registered user of TheHindu Businessline and logged in, you may continue to engage with our articles. If you do not have an account please register and login to post comments. Users can access their older comments by logging into their accounts on Vuukle.