Kumar, a tax manager in a large multinational, returned to office after an enjoyable New Year vacation, feeling refreshed and rejuvenated. While sorting mails he came across a brown envelope containing a notice from the service tax authorities asking his company to provide reasons for the decline in service tax payments. What a start to the New Year!

This, however, is not a stray incident as numerous assessees have received similar notices at the beginning of the year.

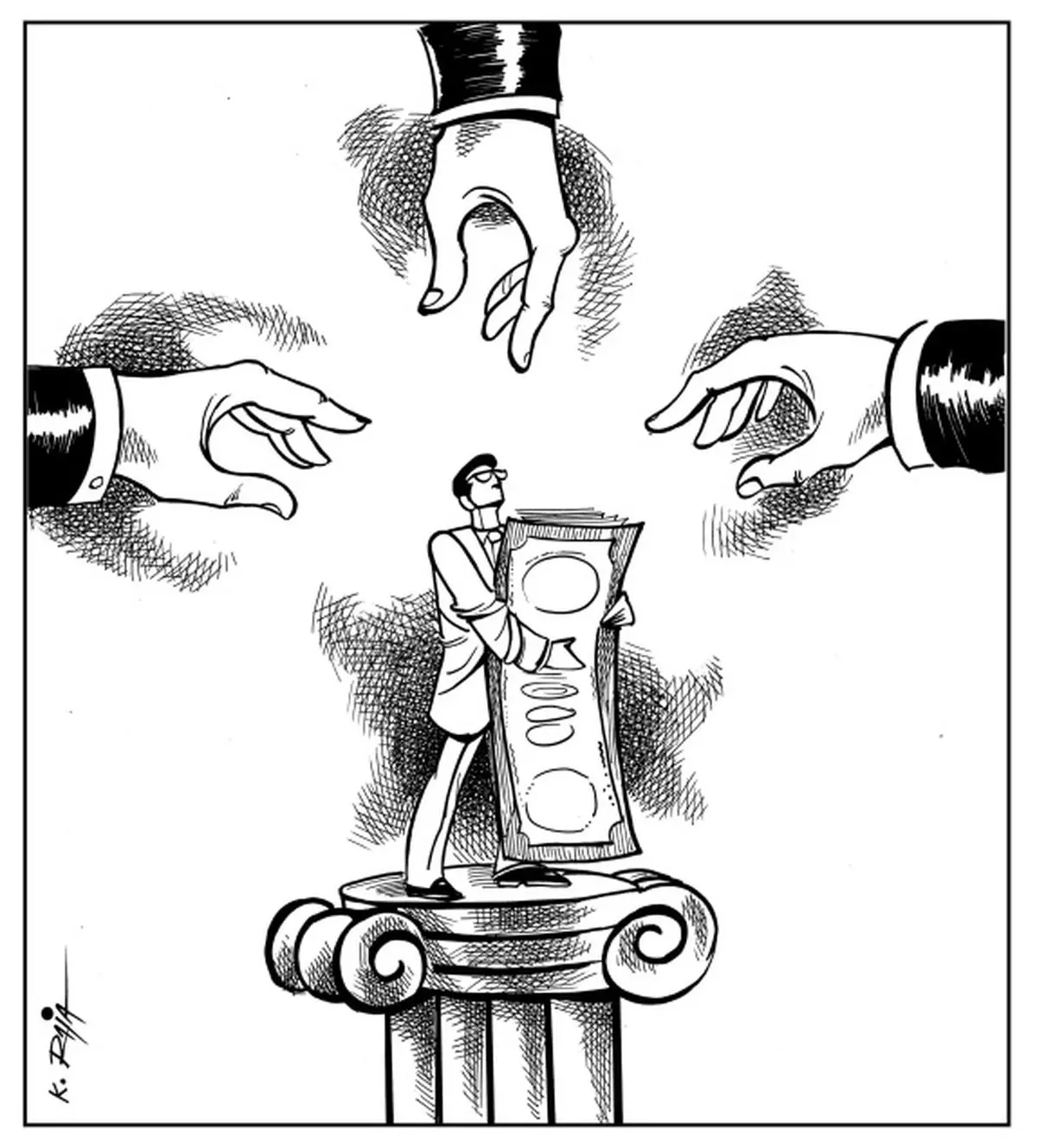

Given the revenue compulsions and with a view to augment compliance and collections in the recent past, the number of notices, audits and various tax/ duty evasion proceedings has increased manifold.

The indirect tax arena involves several legislations, with the revenue to the Centre mainly coming from Customs, Central Excise and Service tax. An entity involved in multifarious activities, including manufacture of goods (where imported raw material and capital equipment may be used), and also engaged in provision of services would need to comply with all the above laws besides Value Added tax, Central Sales tax and Entry tax among others.

Though indirect tax laws require an assessee to self-assess the tax liability, there are checks and balances in the form of audit, assessment and scrutiny by various tax departments. For instance, a service provider apart from assessing and discharging the tax liability suo motu and filing appropriate returns may be subjected to a service tax audit, an audit initiated by the Comptroller and Auditor General of India, a possible special audit and, in some cases, enquiries by the anti-evasion team and/or the office of Directorate General of Central Excise Intelligence. It would be similar under the Customs and Excise laws as well. Also, if the manufacturer is an importer, post-assessment and discharge of duty liability under the Customs Act, an “onsite post-clearance audit” may be undertaken by the department. All this may be in addition to the numerous audits and scrutiny proceedings prescribed under the State VAT and CST laws. Experience suggests that mostly every form of audit results in the issue of a show cause notice and, thus, sets in motion a litigation process winding its way up from adjudication to the Tribunal and Courts. The delay in the adjudication process and the pendency at the appellate stages are mind boggling. Given the rate of disposal vis-à-vis the fresh inflow of notices as service tax coverage increases, the pending matters may take several decades to be cleared. This does not augur well for business, and adds to the uncertainty. The pendency of matters at various levels is not restricted to demands but also on account of rejection of credit refunds in export of services. This adds to the transaction cost and virtually means export of taxes, thereby placing Indian business at a disadvantage.

The multiple audits and investigations by tax authorities indicates a clear dichotomy between the tax administration and the progressive business policy of the Government to attract increased investment

As the current situation is largely writ with uncertainty owing to the conflict between tax administration and policy prescriptions, businesses should adopt prudent practices and take tax positions based on sound reasoning. At the same time, compliances should be regularly monitored, and records and supporting documents should be backed by a sound indexing and retrieval system. Wherever possible the benefit of “advance ruling” and similar such provisions should be utilised to avert uncertainty in indirect tax and possible claim of “back duties/ taxes” with mandatory penalties.

At present, businesses are distracted by the numerous enquiries, audits, litigations. The need is to restore confidence through mechanisms to reduce uncertainty and clarifications on emerging issues.

The author is Senior Director with Deloitte Touche Tohmatsu India Pvt Ltd

![]() Comments

Comments

Comments

Comments have to be in English, and in full sentences. They cannot be abusive or personal. Please abide by our community guidelines for posting your comments.

We have migrated to a new commenting platform. If you are already a registered user of TheHindu Businessline and logged in, you may continue to engage with our articles. If you do not have an account please register and login to post comments. Users can access their older comments by logging into their accounts on Vuukle.