There’s no doubt that the election of Donald Trump as the next President of the United States sets the stage for further expansion of fossil fuel production in the US, especially of natural gas, of which the US has emerged as the world’s largest producer and exporter.

The Ukraine War was a significant catalyst for this, as European countries that were earlier heavily reliant on natural gas from Russia to power their electricity generation desperately sought alternative sources after the US and the EU both imposed sanctions on Russia.

Indeed, analysts pointed out at the time that at least two sectors of the US economy were major beneficiaries of that war: the military-industrial complex, which benefited from huge contracts for the arms that the US supplied as aid to Ukraine (along with arms to Israel); and natural gas producers, who gained from the enforced shift of European demand away from Russia to the US.

Before the Ukraine war, Russia provided gas through a pipeline to western Europe that accounted for around 40 per cent of EU gas imports in 2021. By 2023, that proportion had fallen to only around 8 per cent (EC, Council of the European Union).

If both pipeline gas and liquefied natural gas (LNG) are added together, Russia still provided less than 15 per cent of the EU’s gas imports. In 2023, LNG from the US and Norway provided the bulk of European gas imports.

But recent trends suggest that a more complex picture has been emerging for the global natural gas market since then. It is worth considering the significance of natural gas in total energy sources.

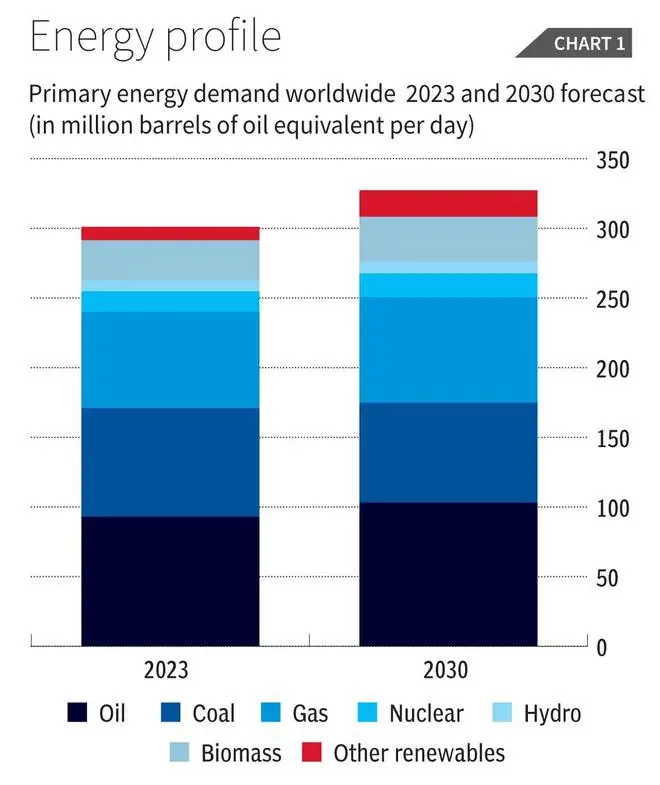

In 2023, natural gas accounted for 22.9 per cent of primary energy demand (Figure 1) and its share is projected to rise to 23.2 per cent in 2030. So it remains an important source of energy globally, after oil (which remains the largest) and then coal (whose share is projected to decline).

Price volatility

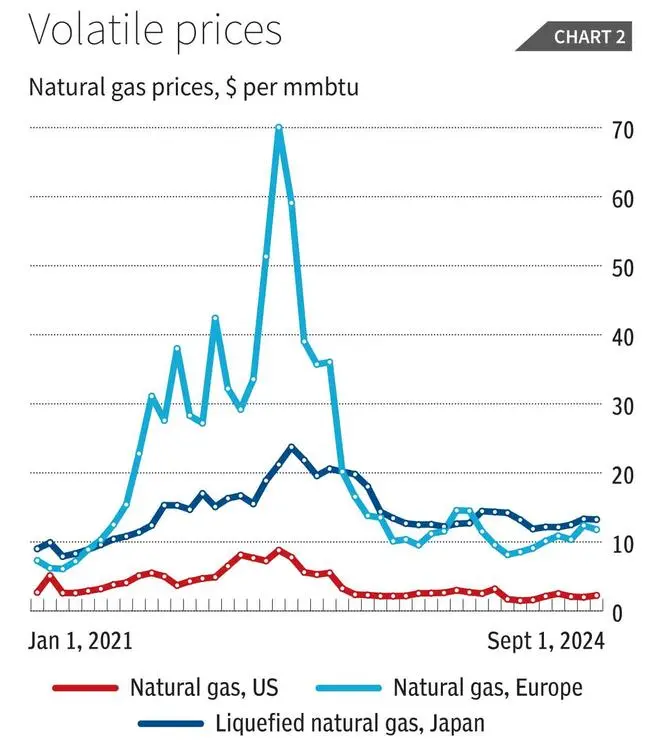

Yet the prices have been extremely volatile over the past few years as indicated in Figure 2 —particularly for Europe, which experienced a dramatic spike in prices in July-August 2022, as the war-related sanctions bit. These increases were also associated with rising prices of transport and energy utilities in several European countries, leading to widespread public anger, and evidently now political fallout as well.

The differences in natural gas prices between the US and Europe are truly remarkable and would be most surprising for any remaining believers in competitive markets.

At the start of 2022, prices in Europe were 6.5 times higher than in the US; by July they were eight times higher. Yet even as prices came down in both countries after August 2022, they declined more steeply and rapidly in Europe, such that by January 2024, prices in Europe were only three times higher than in the US. Nevertheless the price difference remains notable, and cannot be explained by transport costs.

The substitution away from Russia as the source of imports was what was originally associated with the dramatic price increase in Europe, but the subsequent decline in prices was only partly due to the shift to other sources like the US and Norway.

Demand dip

In fact, a possibly greater role was played by an overall decline in demand in Europe. This was partly because of lower economic growth in Europe, especially Germany, along with the attempt to shift to other sources of energy.

Meanwhile, an unseasonably warm winter (part of the broader trend of global warming) meant less need for heating which is a major source of demand for fuel. Figure 3 shows that there was a significant decline in demand for natural gas in Europe in 2022, which also continues into 2024, although to a smaller extent.

This contributed substantially to the decline in global demand for natural gas in 2022. Global demand for natural gas is projected to recover in 2024, but decline slightly once again in 2025.

Supply dynamics

The sources of supply provide an even more interesting story. In 2022, the collapse of supply from Eurasia (including Russia) was more than compensated for, mainly by North America and to a lesser extent by the Middle Eastern region.

But in 2023, supplies from both North America and the Middle East shrunk quite sharply, even as Eurasian gas supplies continued to decline. Despite this shrinkage, and an apparent increase in global demand in 2023 compared to the previous year, natural gas prices in the US and Europe continued to fall, as was shown in Figure 2.

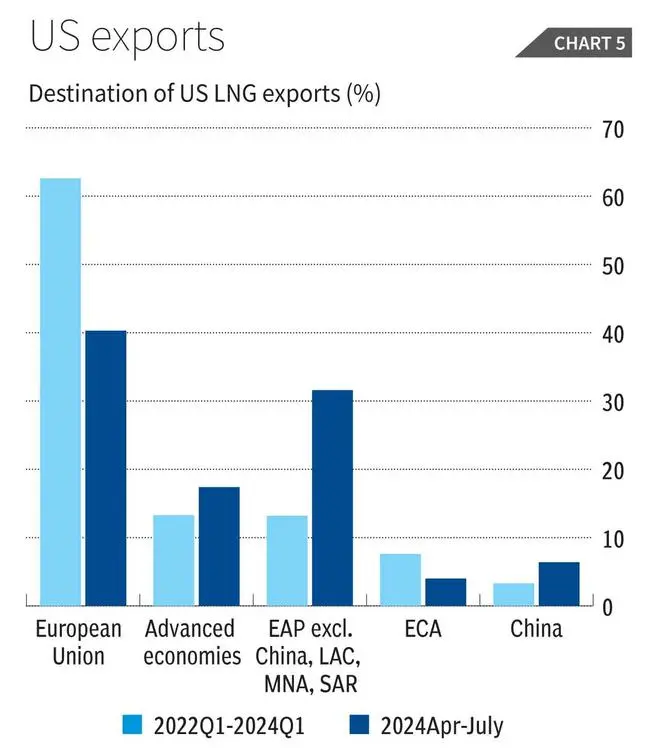

Meanwhile, the US has managed to diversify its natural gas exports to other countries beyond Europe — mainly to developing countries in Asia, the MENA region and Latin America.

Figure 5 shows that the share of US natural gas exports going to the European Union fell from more than 60 per cent in 2022Q1-2024Q1 to around 40 per cent in the most recently available quarterly data, for 2024Q2. Most of this slack was taken up by the developing regions just mentioned.

Movements in the global natural gas market therefore likely reflect both geopolitical pressures and economic forces. It will be interesting to see how the new US administration chooses to navigate this complex terrain in the coming years, given the greater likelihood of “deals” with Russia and the ongoing diversification of US gas exports.

![]() Comments

Comments

Comments

Comments have to be in English, and in full sentences. They cannot be abusive or personal. Please abide by our community guidelines for posting your comments.

We have migrated to a new commenting platform. If you are already a registered user of TheHindu Businessline and logged in, you may continue to engage with our articles. If you do not have an account please register and login to post comments. Users can access their older comments by logging into their accounts on Vuukle.