The race to launch a Central Bank Digital Currency is getting intense with most countries now throwing their hats in the ring. According to Atlantic Council Digital Currency tracker, 105 countries accounting for 95 per cent of the global GDP are exploring a CBDC in some form or the other.

The RBI has been researching the viability of a CBDC over the last few years and has now moved to the development stage with the concept paper which lays the ground for e-rupee. As the paper explains, “The e-rupee will provide an additional option to the currently available forms of money. It is substantially not different from banknotes, but being digital it is likely to be easier, faster and cheaper.”

So, the e-rupee is being envisaged as another form of digital payment option besides UPI, NEFT, IMPS etc and will be as close to physical currency as possible. When we had written about CBDC in March, “Why central bank digital currency can wait,” we had argued that launching an official digital currency for retail use may be risky at this juncture and that a wholesale CBDC can be considered first.

There are obvious operational and cost benefits in launching CBDC in the wholesale (interbank and related wholesale transactions) segment. Besides they could also become the future of cross-border payments.

Cross-border payments

RBI’s hand is perhaps being forced in expediting the CBDC project because other emerging economies are taking the lead in this sphere, even as the advanced economies are going slow. Of the G20 countries, 19 are exploring a CBDC and 16 are in development or pilot stage.

China is showing surprising alacrity; it was among the first to begin pilot testing in 2020 and intends to expand the pilot in 2023. If China, India’s largest trading partner begins using digital currency for domestic and then for external trade, India cannot afford to lag too far behind.

After the Russia-Ukraine war, many countries are actively exploring alternative payment mechanism for international trade and CBDC can facilitate this shift. There are currently nine cross-border wholesale (bank-to- bank) CBDC tests and three cross-border retail (payments between individuals) projects currently in progress. India needs to be ready to participate in these alternative channels when the transition begins.

Interestingly, the US and the UK with the most dominant reserve currencies do not seem to be in a hurry to launch a CBDC. It is apparent that if the world shifts towards digital currencies for cross-border payments and trade settlements, the pole position of dollar and other reserve currencies could be threatened. That will take away their liberty to print unlimited currency notes.

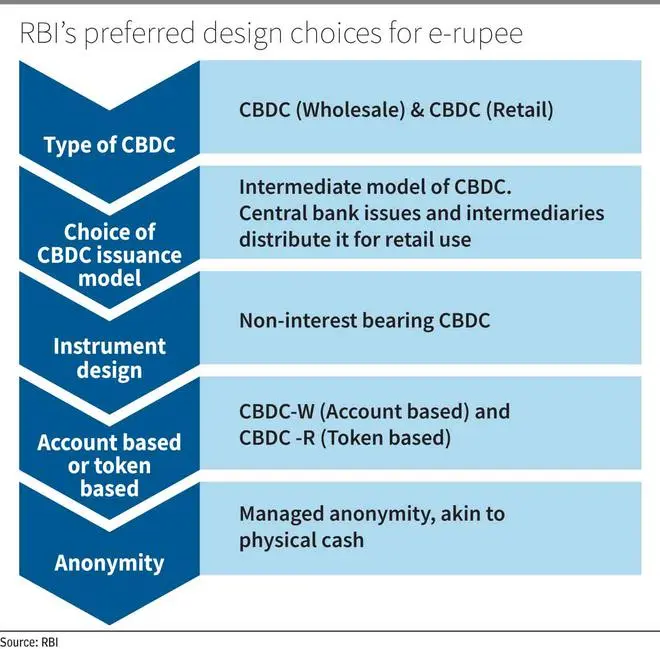

The design conceptualised

Before we move any further, let’s look at the design that RBI is veering towards for the e-rupee.

The RBI has indicated the preferred design choices for the e-rupee, which is shown in the adjacent diagram. The e-rupee will be launched both for retail, and for wholesale segment. It will be a direct liability of the central bank, like fiat currency but will be distributed through banks and other intermediaries. These intermediaries will help in on-boarding clients, providing digital wallets etc and servicing them. The e-rupee accounts will not be interest bearing and therefore will not have too much implication for monetary policy.

The wholesale e-rupee will be account based, where the funds are held in bank accounts. Anonymity will be absent here. RBI is however considering token-based model for retail CBDC, but these could be restricted to only small-value transactions as is being done with CBDCs in Bahamas, China and East Caribbean Union.

Retail CBDC: The hurdles

As discussed above, there are reasons why CBDC in wholesale segment may be needed and can prove beneficial. But the same can not be said of retail CBDC. The primary question is whether they are necessary given the manifold increase in UPI transactions in recent years. There are around 26 crore unique UPI users now and these transactions account for over 65 per cent of digital transactions currently.

There are some ways in which e-rupee is superior to UPI — it is guaranteed by the central bank and does not carry any settlement risk. The load on inter-bank settlement will also reduce with e-rupee.

But given the investment already made in UPI, which is winning global plaudits for the scale and efficiency, does it make sense to introduce another payment system which could cannibalise it? With the introduction of UPI on feature phones and other user-friendly versions, efforts are being made to increase usage of UPI. This may not be the right time to upset the apple-cart.

Two, there is resistance in many segments to switching to digital payment modes. As the RBI concept paper points out, demand for cash has not come down with growing digitisation with value of banknotes increasing 16.8 per cent in F21 and 9.9 per cent in FY22.

People preferring cash for small value transactions could be a reason, but other factors such as illiteracy, affordability and black money holdings could also be driving cash demand. Only a quarter of the mobile phone users in India have begun using UPI.

The RBI’s plan to offer e-rupee in offline mode is touted to help financial inclusion, but willingness to switch away from cash is needed to make this work. Developing an underlying technology which is secure and protects consumer interest will be a challenge too.

Take it slow

The actual impact of CBDC on financial system and economy is however yet to be seen. Of the 11 countries which have launched official digital currencies, 10 are relatively small countries of Eastern Caribbean, Bahamas and Jamaica. Nigeria is the only large country to have launched CBDC for retail use in October 2021. RBI will therefore have to move extremely cautiously in pilot testing and introducing the CBDC.

![]() Comments

Comments

Comments

Comments have to be in English, and in full sentences. They cannot be abusive or personal. Please abide by our community guidelines for posting your comments.

We have migrated to a new commenting platform. If you are already a registered user of TheHindu Businessline and logged in, you may continue to engage with our articles. If you do not have an account please register and login to post comments. Users can access their older comments by logging into their accounts on Vuukle.