Consider these four recent statements/news reports:

The RBI to hike repo rate on high WPI inflation, feels Street — headlines one financial newspaper.

The repo rate is immaterial and should be thrown out, says recently retired SBI Chairman in an interview. Repo rate moves have negligible impact on bank deposit and lending rates, he says.

The Finance Ministry wants public sector banks to cut lending rates and expand consumer lending; that will increase consumption expenditure and thereby boost economic growth, it says.

RBI Governor Raghuram Rajan says that using interest rates to tackle high inflation in India is more complicated in India than in the US — because a large part of the country is not connected to the formal financial system.

You will not be wrong if you think that each statement squarely contradicts its immediately preceding one; for instance, “b” contradicts “a” and “d” contradicts both “c” and “a”.

If repo rate moves barely impact deposit and lending rates, how can raising them push down inflation at all?

Further, if lower interest rates can boost consumption and growth, higher interest rates should do the opposite — that is, restrict demand and moderate pricing pressures.

So, which one is correct?

Answering that question will throw light on two key areas of economic/central bank policy.

To sort this out, the RBI has recently appointed two committees — one, to design a monetary policy framework and another to formulate an institutional framework for attaining financial inclusion and deepening in India.

Further, extrapolating from the comments of the Governor, the work of the two committees could well converge; if the financial inclusion committee’s design framework is able to bring in the unconnected parts of the country into the formal financial system, the efficacy of the monetary policy framework is automatically strengthened.

RBI’s challenge

You cannot get a stronger repudiation of the extreme short-termism in market reactions to developments in the macro-economy than the former SBI Chairman’s statement.

Indeed, if the latest WPI number had come in a shade lower, the “Street” would have sounded the all-clear for a reduction in the repo rate. Such is the fixation on the short-term. The policy recommendation is data release to data release.

A perspective on how central bank interest rate moves impact banks’ deposit and lending rates is not obtained in the process; and, in turn, how they influence consumption, savings and investment behaviour in the economy over a period of time.

With his hard-hitting comments, therefore, the ex-SBI Chairman may have done a signal service in highlighting the RBI’s challenges.

Provision of liquidity, at the margin, to the financial system at a certain cost, tenor and quantum — either through a discount window as in the US or through a system of daily liquidity auctions as the RBI does, is a well-known tool of monetary policy implementation.

By altering the cost, tenor and quantum of liquidity, the central bank influences the broader structure of interest rates, starting with banks’ deposit and lending rates.

Therefore, why does the ex-SBI Chairman completely write-off the RBI’s repo rate mechanism as having no impact on broader interest rates?

The flaw seems to be with the technique adopted by the RBI in its repo operations. Note that for any bank, an intervention rate such as the repo rate plays a role, only in conjunction with other forces in influencing its deposit rates. Those forces are primarily market competition, balance-sheet composition and liquidity considerations.

Therefore, when the RBI seeks to influence the system’s deposit pricing, its repo rate moves must have an impact on those forces. At any point in time, not all banks borrow at the repo window.

There are both liquidity deficit and liquidity surplus banks in the system. (Deficit banks’ first recourse is the inter-bank market. Only after exhausting that do they go to the repo window). But for borrowings at the repo window, the repo rate should be at such a level/or the quantum of liquidity support should be such that it impacts those other forces (noted above).

For instance, repo liquidity should be available at some rate ‘x’ but that ‘x’ should compel the borrower to adjust (significantly) his deposit rates; that, in turn, can potentially set off competitive forces in the market, taking overall deposit rates up. (Same concept should apply when reverse repo is used to signal lower rates).

Note that the magnitude of moves in the repo rate and in banks’ deposit rate(s) need not be the same. The repo move, at the minimum, though, has to spark off competitive forces in the market. The repo rate, at the minimum, also has to be higher than the maximum deposit rate(s) on offer.

The ex-SBI Chairman’s statement shows that the RBI’s moves so far are not doing that. The RBI just keeps supplying liquidity at ongoing market rates and, therefore, there is no impact at the system level.

(At a more fundamental level, the repo is also rendered meaningless in the face of large RBI balance-sheet expansion).

Financial exclusion

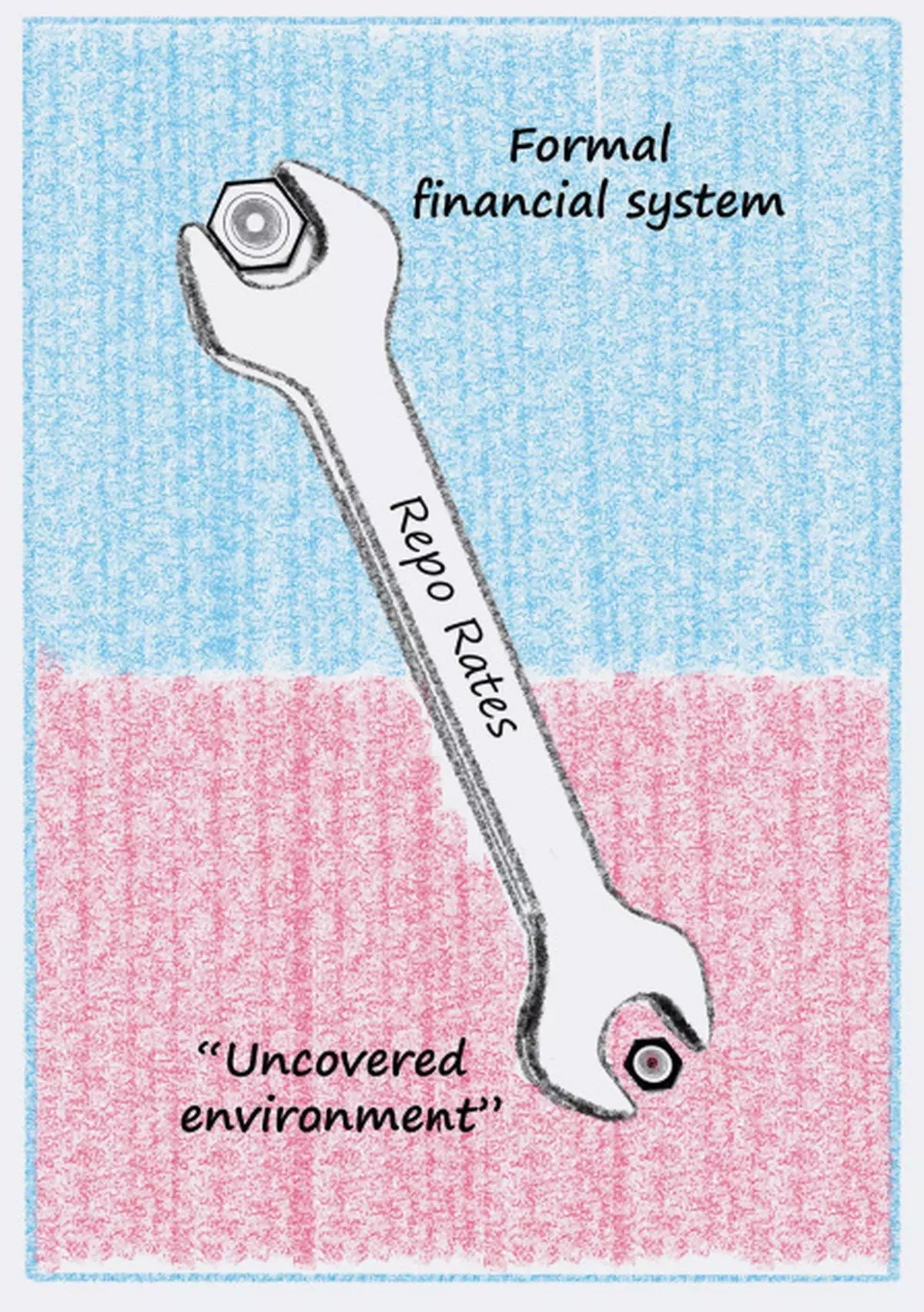

Another key point is the level of financial exclusion in India and whether interest rate moves are relevant in that scenario.

To be sure, the excluded sections do not directly constitute the “interest rate sensitive sectors”. But, if 50 per cent of the country is covered by the formal financial system, changes in the “covered environment” are bound to spill over into the “uncovered environment” — even if competitive forces are largely absent in that “uncovered environment” and borrowers, therefore, are at the mercy of lenders (evidenced by the significant role of local money-lenders in India).

The challenge then is to design an institutional framework to attain financial inclusion and thereby enhance policy effectiveness.

(The author is a Chennai-based financial consultant.)

![]() Comments

Comments

Comments

Comments have to be in English, and in full sentences. They cannot be abusive or personal. Please abide by our community guidelines for posting your comments.

We have migrated to a new commenting platform. If you are already a registered user of TheHindu Businessline and logged in, you may continue to engage with our articles. If you do not have an account please register and login to post comments. Users can access their older comments by logging into their accounts on Vuukle.