India’s foreign direct investment (FDI) scenario has witnessed a disquieting shift, with recent figures raising alarm about the nation’s ability to sustain its attractiveness to global investors. Net FDI inflows at $9.8 billion in FY24 were sharply below $28 billion in FY23.

While it is true that global FDI flows have been on a downturn, with Unctad’s World Investment Report 2024 noting a drop from $1.62 trillion in 2021 to $1.33 trillion in 2023, India’s situation appears more dire.

India’s share in global FDI flows has seen a steep decline in recent times, dropping from 6.6 per cent in 2020 to just 2.2 per cent in 2023. This decline is particularly stark when considered against the much-touted “China plus one” strategy, which was expected to redirect significant FDI towards India. Clearly, the plan has not materialized as anticipated. While China’s share of global FDI inflows decreased significantly from 12.5% to 1.7% between 2022 and 2023, India failed to capitalize on this shift.

The underperformance is further underscored by India’s slide in FDI destination rankings, from sixth place in 2020 to 15th in 2023, while peers like China and Brazil have strengthened their positions. This regression, viewed against the country’s previous upward trajectory in the post-liberalization period, signals deeper systemic issues not adequately addressed by current policies. The latest budgetary measures, while commendable in their intent to simplify FDI regulations and reduce corporate tax rates for foreign companies, fall short of the pragmatic stance needed to reverse the downward trend in FDI inflows.

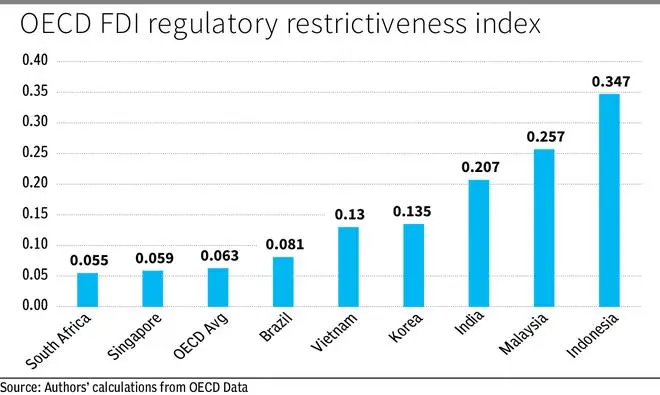

The challenges are manifold. First, despite improvements in some areas, India’s policy environment continues to lag behind its peers in creating a truly investor-friendly climate. For instance, the OECD’s FDI Regulatory Restrictiveness Index shows that India’s FDI restrictions remain higher (0.207) than rivals like Vietnam (0.130), South Africa (0.055), Brazil (0.081), and Korea (0.135) (see figure).

BIT issues

Second, India’s decision to terminate or renegotiate the majority of Bilateral Investment Treaties (BITs), ostensibly aimed at protecting national interests, may have inadvertently signalled policy unpredictability, severely denting investor confidence. The 2016 BIT model, which emphasised regulatory power over investor protections and imposed lengthy domestic dispute resolution requirements before allowing international arbitration, has found few takers among India’s key trading partners.

Global investors are wary of committing long-term capital, fearing inadequate protection for their investments. This hesitance has hindered the signing of new treaties and has become a significant impediment in broader trade negotiations, including free trade agreements.

Third, the stagnation in Sustainable Development Goals (SDG)-related investments, as highlighted by the World Investment Report 2024, adds another layer of complexity to India’s FDI landscape.

As global capital increasingly seeks out sustainable and impact-driven opportunities, India must position itself as a leader in this space. This calls for a concerted effort to align national development goals with global sustainability standards, making the country an attractive destination for long-term responsible investment.

To attract more FDI, India must further liberalise key sectors such as insurance, e-commerce, and multi-brand retail.

Comparative advantage

Besides, India needs to focus on sectors where it possesses comparative advantage, such as renewable energy and digital technologies. By aligning FDI policies with these strengths, India can create a more targeted and effective approach to attracting foreign capital. The sectoral focus should be complemented by efforts to strengthen institutional capacity to better facilitate and retain foreign investments, ensuring that initial investments translate into long-term commitments.

A key priority must be the enhancement of digital government services to streamline business processes and improve transparency.

The government must prioritize creating a more transparent, predictable investment climate.

Sur is economics faculty, Jindal Global Law School, O P Jindal Global University; Nandy is economics faculty, IIM Ranchi. Views are personal.

![]() Comments

Comments

Comments

Comments have to be in English, and in full sentences. They cannot be abusive or personal. Please abide by our community guidelines for posting your comments.

We have migrated to a new commenting platform. If you are already a registered user of TheHindu Businessline and logged in, you may continue to engage with our articles. If you do not have an account please register and login to post comments. Users can access their older comments by logging into their accounts on Vuukle.