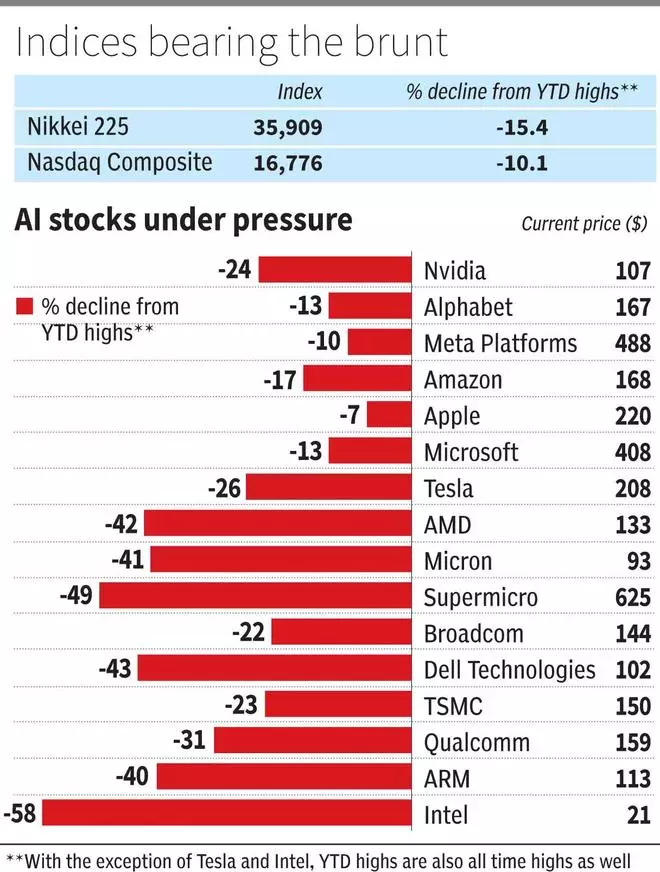

As of Friday’s close, Japan’s Nikkei 225 is down 15 per cent from its all-time highs reached a just few weeks back, on July 11. Its 5.8 per cent decline on Friday is one of its worst single day decline ever.

And if the follow through were to sustain on Monday’s opening — as indicated by the Nikkei Futures trading down by another 5 per cent following weak economic data from the US on Friday — it could be knocking on the doors of a bear market in less than a month from its peak.

Across the Pacific, the Nasdaq Composite entered correction territory on Friday, having fallen more than 10 per cent from its peak of 18,671 on July 11. The Magnificent Seven and many other AI stocks are already either in deep bear market or correction territory.

Add to this, the spike in the volatility index in the US represented by CBOE VIX (called the ‘fear gauge’) during the course of Friday by as much as a staggering 60 per cent.

While it did recover, at its closing price of 23.39, it is now trading around the levels where it was when Silicon Valley Bank and Credit Suisse folded up.

Three factors are driving this turbulence.

AI economics

The billions of dollars spent by companies like Microsoft, Alphabet and Amazon in building AI Hyperscalers for either developing proprietary capabilities or to expand cloud service business has all of a sudden become investor discomfort.

Nearly two years after the launch of Chat GPT and more than a year after Nvidia’s results ignited the AI rally, the economics of AI remain unclear.

While the views of experts are divided given no transformative changes due to AI yet, one consensus that is emerging is that the benefits of investing will take a long time to yield monetary results and justify the economics of large outlays. Investors are now beginning to factor this.

Tesla’s Q2 results were disappointing. On the other hand, Alphabet, Microsoft and Amazon’s results/outlook were modestly below expectation. However, given the optimism baked into the shares on AI potential, these were triggers for a correction.

Unwinding of yen carry trade

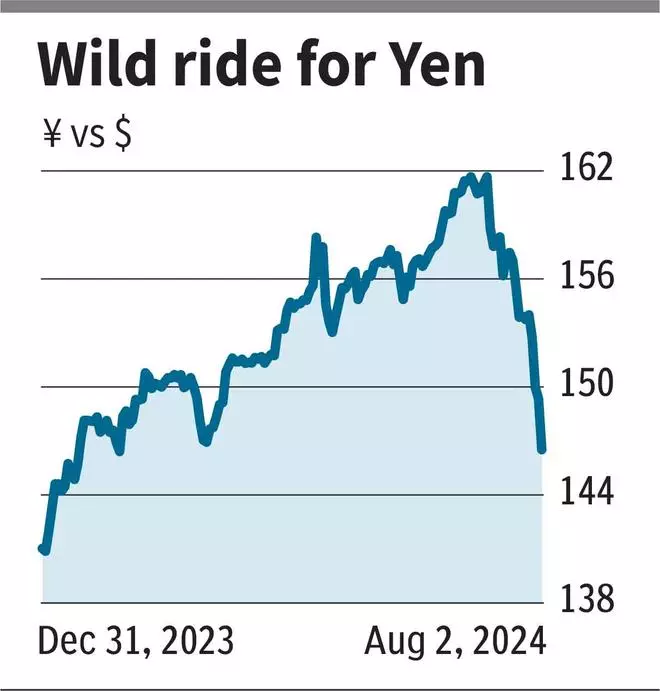

During the course of this year, the Japanese yen fell by nearly 14 per cent to 161.6 against the US dollar to reach its lowest levels since 1986. Since reaching that bottom on July 10, currency intervention and rate hikes by the Japanese central bank, Bank of Japan, along with hawkish messaging by its Governor Kazuo Ueada, triggered a 9 per cent up move to 146.9, with most of the gains concentrated in the last few days.

A weak Japanese yen for long has been a tool for the global yen carry trade where investors borrow in yen (given its weakness and low borrowing costs) and invest in other assets — equities, higher yield government debt like that of the US and stronger currencies. The arbitrage was theirs to pocket, with the only risk being an appreciation in the yen which would eat into their profits or result in outright losses.

So the sudden surge in the yen in recent weeks seems to have caused a large-scale unwinding in the carry trade, that is, investors sell their other assets to repay their yen borrowings.

In the process, the other assets, including equities, have been under pressure last week.

Sahm Rule red flag

Global markets got another shock from the US monthly jobs report released on Friday, which indicated the unemployment rate had increased to 4.3 per cent.

While still remaining amongst the lowest level, it spooked markets because at 4.3 per cent, it triggered the ‘Sahm Rule’.

This rule states that when the three-month average of the unemployment rate is 0.5 bps above its 12-month low, a recession is underway.

Historically, it has been a very accurate indicator. Friday’s chaotic move across equities, bonds and fear gauge was due to this single factor.

What next?

The irony though is that Claudia Sahm, the economist who created the Sahm Rule, was on record yesterday noting that ‘this time it could be different’ due to few specific factors and that the economy may not be in a recession,although she believes it is slowing to concerning levels.

Further, a few others have pointed out that the Sahm Rule was triggered due to rounding off of decimals!

Nevertheless, heightened uncertainty prevails, with recent tensions in the Middle East adding to risks to markets from worsening geopolitics.

Recession or not, turbulent global economy and financial markets is not good news for Indian markets. US recessions in the past have always resulted in deep bear markets in India as well.

With markets at peak valuations when risks abound, strong domestic macros may not be a sufficient cushion.

![]() Comments

Comments

Comments

Comments have to be in English, and in full sentences. They cannot be abusive or personal. Please abide by our community guidelines for posting your comments.

We have migrated to a new commenting platform. If you are already a registered user of TheHindu Businessline and logged in, you may continue to engage with our articles. If you do not have an account please register and login to post comments. Users can access their older comments by logging into their accounts on Vuukle.