2022 was the worst year for the Indian rupee since 2013. While then it was a combination of global (taper tantrum) and domestic factors (high inflation), this time it was primarily driven by global factors. Thus, after witnessing a few years of calm with gradual 2 per cent average fall against the dollar for three consecutive years, the domestic currency experienced a storm in 2022 and tumbled by 10 per cent to close at 82.74.

A lot changed in 2022

First, it is the strength of the dollar. The US Federal Reserve’s aggressive rate hikes all through 2022 saw the US Treasury yields surging higher. The US 10 Yr Treasury yields surged from around 1.5 per cent in December 2021 to 3.8 per cent by the end of 2022. As a result, the dollar index skyrocketed 20 per cent to make a twenty-year high of 114.78 in September last year, the levels last seen two decades back in May 2002. Thereafter the index had come off to close the year at 103.51, up 8.21 per cent in 2022.

Second, crude oil prices spiking above $100 per barrel weighed on the rupee. The outbreak of the Russia-Ukraine war in February took the Brent Crude oil prices to a high of $140 per barrel in March. The oil prices continued to hover higher above $100 until June. Oil being the major import component for India, higher prices increased the country’s import bill and, in turn, widened the trade deficit. India’s monthly oil imports increased from $16.45 billion in December 2021 to $21.5 billion in June 2022. Trade deficit widened from $21 billion to $24 billion over the same period.

Finally, strong foreign money outflow from the country was the third factor that caused the rupee depreciation last year. Foreign Portfolio Investors (FPIs) were net sellers of both the debt and equity segment last year. The equity segment saw a net outflow of about $17 billion and the debt segment about $2 billion. Dollar strength, flight to safety amidst slowdown fears and relative overvaluation of Indian markets versus other emerging and developed market peers, were the likely reasons driving the outflows.

2023 - What’s ahead

After a volatile year 2022, the new year 2023 could provide some respite for the Indian rupee. Most the of the factors that caused dollar strength/rupee weakness in 2022 are likely to persist in the first half of 2023 as well. However, since all the risks are largely factored in the market already, the impact on the rupee could be less destructive. As such, in the absence of any new event risk, the rupee can stage a recovery in the second half of 2023. Here we take a look at that factors that are for and against the rupee in 2023.

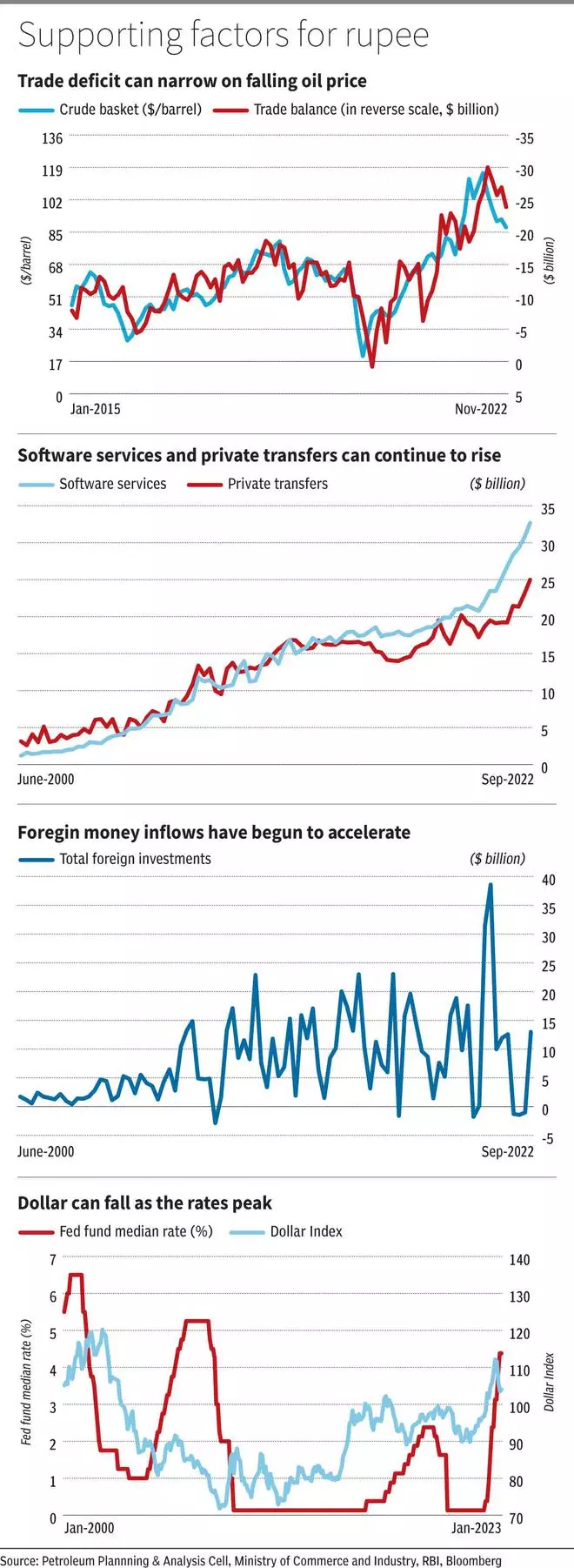

Factors supporting rupee

Cooling oil price

Crude oil prices falling and sustaining well below $100 is a positive. This has spelt a significant relief of late for the country’s oil import bill. On an average, crude oil imports form about 30 per cent of the country’s total imports.

India’s crude basket has come down from an average of $103 per barrel in the first half of 2022 to about $78 per barrel in December 2022. India’s oil imports cost stood at $15.74 billion in November 2022, down about 15 per cent from an average of $18.5 billion in the first half of 2022. However, the import cost is still much higher than the average of $8.8 billion seen in the calendar year 2021.

Crude oil prices are likely to remain lower in 2023 on the back of a possible slowdown in the global economy. The International Energy Agency (IEA) expects the world oil demand to fall by 1.7 million barrels per day (mb/d) in 2023 as compared to an increase of 2.3 mb/d in 2022. The US Energy Information Administration (EIA) projects the Brent Crude to average around $92 per barrel in 2023.

On the charts, the outlook for Brent Crude oil ($83) is weak. It can fall to $70-$65 from here. The broad range of trade for 2023 could be $65-$95.

CAD, BoP can improve

The fall in crude price below $100 has already aided in narrowing down the merchandise trade deficit — from around $30 billion in July to $24 billion in November last year. A further fall in oil price from here can see the trade deficit narrowing even more to about $20 billion in the coming months.

Software services exports and private transfers form a major part of the invisibles component of the current account. Software services have increased from $28.35 billion in December 2021 to $32.68 billion in September 2022. Private transfers, on the other hand, have gone up from $21.45 billion to $25 billion over the same period. As the rupee continues to remain below 80, both software services and the private transfers can continue to increase further.

So, a narrowing trade deficit on the back of low oil prices, coupled with an increase in the invisibles, in the form of software services exports and private transfers, can aid in improving the Current Account Deficit (CAD) in 2023. As per the recent data released by the Reserve Bank of India, our CAD is at $36.39 billion as of September 2022.

On the Capital Account front, the foreign money flows have started to improve in the recent months. RBI’s data shows that the total foreign investments, that is the Foreign Direct Investment (FDI) plus the Foreign Portfolio Investments (FPI), have increased from $1.03 billion in June 2022 to $12.97 billion in September 2022. Recent data from the National Securities Depository Limited (NSDL) shows that there has been a net inflow of about $5.38 billion from Foreign Portfolio Investors (FPIs) in the last two months of 2022. The Capital Account surplus, which has come down to $6.92 billion in September from around $28 billion in June last year, can increase on the back of the improved foreign money inflows.

Rates to peak

Dollar was driven in 2022 majorly on the back of aggressive rate hikes by the US Fed. The US central bank had increased the rates from 0-0.25 per cent to 4.25-4.5 per cent by the end of 2022. This includes four rounds of 75 basis points (bps) increase. This is the first time since 1994 that the US Fed has increased the rates by 75 bps in one meeting.

According to the Fed’s recent economic projections released in December 2022, the median projection for fund rate is forecast to be at 5.1 per cent for 2023. This means that 2023 will get a cumulative rate hike of 75 bps. Thereafter the Fed has projected to cut the rates by 100 bps points each in 2024 and 2025. Assuming that the Fed sticks to these projections, given the inflation in the US has been giving signs of cooling down recently, the interest rates in the US can peak at 5-5.25 per cent and then start to come down.

As seen from the chart, it is evident that the dollar index and the Fed fund rates move in tandem. So, the dollar index can move up as the Fed hikes the rates by another 75-bps, possibly in the first half of the year, and then start to come down.

From the charts, the dollar index (105.15) has good support now near 102. A rise to 108-110 can be seen in the next couple of quarters. Thereafter the dollar index can come down again towards 102 and indeed fall below 100.

Factors against rupee

A couple of factors can be unfavourable for the rupee in 2023. We analyse these below

Recession worries

One important event as of now that might not have been fully factored in the market would be the expected recession in the US in 2023 and an overall global growth slowdown. The International Monetary Fund (IMF), in October 2022, had projected the global growth to slow down to 2.7 per cent in 2023 from a projected growth of 3.2 per cent in 2022. During recession, the dollar usually gains strength. For instance, during the 2001 dotcom recession the dollar index rose from around 108 in January 2001 to 121 in July 2001. During the 2008-2009 great recession, the index rose from a low of 71 to a high of around 89. So, if a recession hits the US in the first half of 2023, the dollar index can rise. But thereafter it can start to fall again.

Though a recession could impact India also, historical data shows that there have been strong foreign money flows into the country from the middle of the recession and they extend for a prolonged period after the recession ends. During the 2008-2009 great recession, the Indian equities saw an outflow of $12 billion in 2008. However, India started to receive inflows into equities from March 2009, well before the recession technically ended in June 2009. The FPIs pumped in a whopping $18 billion into Indian equities from March to December 2009. So, the recession, if it comes, will have a negative impact for a short span of time.

China opening up

China relaxing its Covid restrictions have created jitters in the market. This has increased the fear of another wave of the pandemic. While the impact is not clearly known as of now, it is to be remembered that the markets made a strong and very quick comeback during the first wave of the virus spread. So, assuming the same, any serious impact from fears of another wave spreading will be shortlived.

Reserves build-up

India’s forex reserves had come down significantly in 2023. From $642 billion in September 2021, the reserves had fallen to $524 billion in October 2022. But thereafter the RBI had begun to build up its forex reserves. As of December 23, the forex reserve is at $562 billion. If the RBI decides to build up its reserves by intervening in the forex market as it did in 2021, then the strength in the rupee could be restricted.

Our take on the rupee

Overall, we can expect the dollar to remain strong in the first half of the year on the back of more rate hikes and recessions fears. This can continue to keep the rupee under pressure in the first half of 2023. However, the greenback can lose sheen in the second half of 2023. This, coupled with improving domestic macro-economic conditions such as narrowing trade and current account deficits on the back of low oil prices and improving foreign money flows, can help the rupee to recover in the second half of 2023.

To sum up, the Indian rupee can weaken towards 85 against the dollar in the first half and then recover towards 81-80.

Given this, companies with dollar-denominated loans and higher imported components in their business may continue to face some pressure during the first half of the year. These pressures may fade as the year goes by, unless there is an unexpected global shock. On the other hand, for companies with high export earnings, while currency depreciation, till it continues, ideally should be a positive, this may be offset by the slowdown in developed economies, which can impact their business.

What the charts say

In April last year when the rupee was around 76 against the dollar, we had forecast that it would weaken towards 80-80.50 by the end of 2022. The fall has indeed extended well beyond our target and the rupee made a new low of 83.29 in October last year. The domestic currency has recovered from the low and has been broadly range-bound between 80.50 and 83.29 since then. We now analyse the charts to see where the rupee is headed in 2023.

Source: MetaStock

Short-term view: The current consolidation between 80.50 and 83.29 is likely to remain in place atleast for another month or two. The overall downtrend is intact and there is room for fall within it. Important short-term resistances are at 81.80, 81.50 and at 81.10-81.00. The chances are high for the rupee to remain below 81 in the short term.

We expect the rupee to break the 80.50–83.29 range on the downside. Such a break below 83,29 can take the rupee lower to 84.80-85 and even 85.25-85.50 in the first half of 2023

Long-term view: The levels of 84.80-85.00 and 85.25-85.50 mentioned above are the two major support zones for the rupee in 2023. We can expect the domestic currency to bottom-out in either of these support zones. A strong bounce-back move thereafter can see the rupee recovering towards 81.20-81 and even 80 in the second half of 2023. In case the rupee manages to breach 80, the upside can extend up to 79.50-79.30.

An analysis on the long-term historical movement of the rupee indicates that the recovery from around 85 might have the potential to take the rupee even up to 78.50-77.50 as well. However, it is too early to take a call on this.

So, for now, our preferred path of move for the rupee in 2023 will be to see a fall to 84.80-85.00 or 85.25-85.50 in the first half of the year. Thereafter the currency can recover towards 81.20-81 and 80 in the second half of 2023.

![]() Comments

Comments

Comments

Comments have to be in English, and in full sentences. They cannot be abusive or personal. Please abide by our community guidelines for posting your comments.

We have migrated to a new commenting platform. If you are already a registered user of TheHindu Businessline and logged in, you may continue to engage with our articles. If you do not have an account please register and login to post comments. Users can access their older comments by logging into their accounts on Vuukle.