For a while now, there has been a broad market consensus that interest rates have peaked and that with relatively benign inflation, there may be a possibility of a reduction in rates later in the year. Indeed, after the interim budget of 2024-25, after a healthy fiscal path was laid out, g-sec yields fell sharply to sub-7 per cent levels in February this year. With the inclusion of Indian bonds in the JP Morgan index from this month and a flattening of the yield curve, there is a fair case for long-term duration or constant maturity play. That argument still holds.

However, the election of a coalition government, the likelihood of a more consumption-driven budget and a greater focus on rural income improvement may delay the rate-cut timelines.

A As has been the case in June, a relatively weak progression of the monsoon can aggravate food inflation (which is still in excess of 8 per cent). Given the weightage for food articles in the headline indices, this may cause a surge in overall inflation.

The government’s budget moves would also need to be watched. If there are announcements about increases in direct benefit transfers, farm loan waivers, and higher allocations to rural employment guarantee schemes, apart from any tax concessions, the fiscal path may be altered. A larger deficit may be the recipe for higher inflation.

These factors, such as inflation and fiscal deficit, may force the RBI to go slow on interest rate cuts.

There is also no sign of going back on the stance of ‘withdrawal of accommodation’ from the RBI and it may continue to keep liquidity tight.

In fact, as of June 27, the liquidity deficit in the system was ₹1.52 lakh crore, according to the RBI data. Liquidity has been in the deficit for the whole of June.

Thus, short-term interest rates may still hold up for the foreseeable future. Of course, the same level of returns seen at the short end of the curve in the last couple of years may not be repeated but may still offer a relatively attractive option.

In this regard, ultra-short-term funds can be considered by investors for parking their emergency funds or for short-term goals. The ICICI Prudential Ultra Short-Term fund has been a consistently robust scheme in the category and may be suitable for investors with a moderate risk appetite.

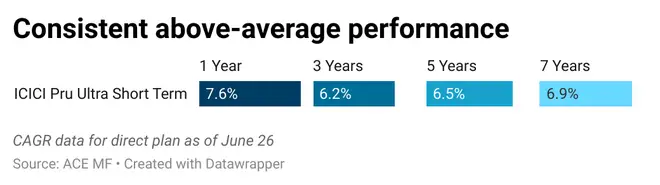

Above-average performance

The fund was earlier called ICICI Prudential MIP 5. Hence, we take the returns data for ICICI Prudential Ultra Short Term from 2018, after the new SEBI criteria on mutual fund classification were operationalised.

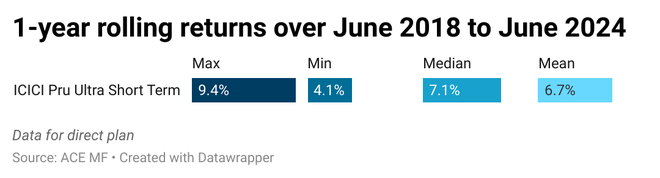

When one-year rolling returns from June 2018 to June 2024 are taken, the fund has delivered an average of 6.7 per cent annually .

Taking the same data mentioned above, the fund has delivered more than 7 per cent returns around half the time and more than 6 per cent returns nearly 64 per cent of the time. The fund has delivered more than 8 per cent over 23 per cent of the time.

A maximum of 9.4 per cent return over 1-year rolling periods from June 2018 to June 2024 and, more importantly, a minimum of 4.1 per cent return mean that the scheme has consistently been an above-average performer.

Safe holdings

Ultra short-term funds are allowed to invest in debt and money market securities in such a way that the Macaulay duration of the portfolio is between 3 and 6 months.

ICICI Ultra Short Term invests in treasury bills, certificates of deposits (CDs), commercial papers (CPs) and corporate securities.

Apart from treasury bills issued by the RBI, the fund invests in the certificates of deposits of Axis Bank, HDFC Bank, NABARD, SIDBI. and Union Bank of India, among others.

The scheme holds commercial papers of Embassy Office Parks REIT, Nuvama Wealth, Sharekhan, and Motilal Oswal Financial Services.

Bharti Telecom, Bajaj Housing Finance and LIC Housing Finance are some of the corporate securities held.

Overall, more than 82 per cent of the securities in its May 2024 portfolio are sovereign or carry the highest AAA or A1+ ratings. About 13.6 per cent of the securities carry AA ratings, but these are securities issued from reputed corporate houses such as Mahindra Rural Housing Finance, Tata Housing Development Company and Motilal Oswal Finvest. Thus, the fund takes almost no credit risk.

The current Macaulay duration is healthy at 0.46 years (less than six months), as is the yield to maturity at 7.72 per cent.

It is worth noting that CPs and CDs of 3-month tenor are still available at yields north of 7 per cent.

Investors can consider the fund for short-term goals for stable returns.

![]() Comments

Comments

Comments

Comments have to be in English, and in full sentences. They cannot be abusive or personal. Please abide by our community guidelines for posting your comments.

We have migrated to a new commenting platform. If you are already a registered user of TheHindu Businessline and logged in, you may continue to engage with our articles. If you do not have an account please register and login to post comments. Users can access their older comments by logging into their accounts on Vuukle.